464 | Using SMSFs to Avoid Getting Stuck on Your Next Property!

Episode description

Many investors can’t seem to move beyond owning 2-properties due to limited borrowing power or equity, so why don’t more people turn to Self-Manager Super Funds (SMSFs) as an answer?

Folks, this is just ONE of the enlightening questions from today’s enormous Q&A episode which has a bit of gold for every property investor, no matter what stage you are at on your property journey.

From the ultimate pros and cons list of SMSFs to revealing the true long-term advantages of owner-occupier appeal – and why it matters over high yield - we’re exploring the winning strategies one can use to move up the property ladder.

We also explore the moral and ethical dilemma of property investing (are you evil if you become a property owner?!?) and do a first-time reveal of our newest series.

Tune in now to hear all this – and how you can access this series for free – and learn how to maximise your returns today! 😊

Free Stuff Mentioned

- Be part of 2023/24 Summer Series (Especially calling all ladies!). Share your story, get a free Start & Build course and positively impact our community today. Reach out to us here >>

- What’s Making Property News: Read the results from PIPA’s Annual Property Investor Sentiment Survey 2023!

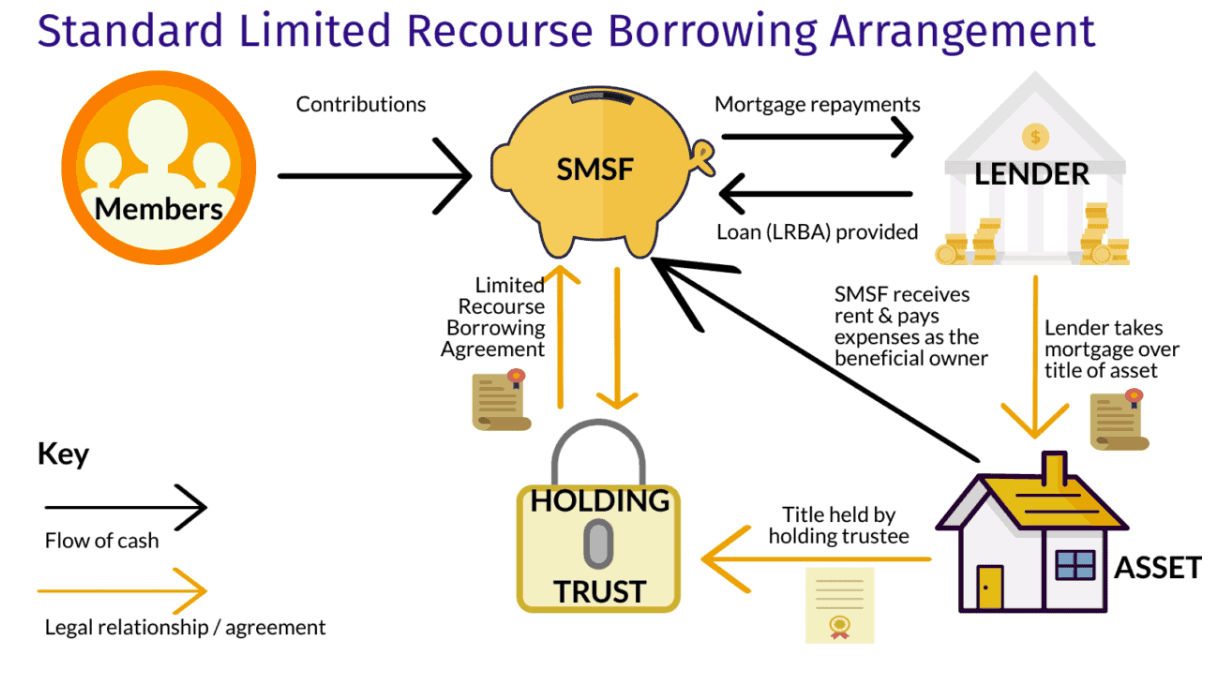

- Q2) See a helpful diagram of how SMSFs work here.

- Previous episodes mentioned:

463 | Property Managers: Are They Worth It?! – Q&A Day

{kind=link}

LISTEN TO THE FIRST 20 EPISODES HERE >>

MOORR MONEY MANAGEMENT APP:

👉 Apple: https://apple.co/3ioICGW

👉 Google Play: https://bit.ly/3OT86bW

👉 Web platform: https://www.moorr.com.au/

FREE MASTERCLASS:

- How to Build a Property Portfolio and Retire on $2,000 a week >>

FREE BEST-SELLING BOOKS:

- The Armchair Guide to Property Investing

- Make Money Simple Again

FIND US HERE:

- Website

- Instagram

- Facebook

- Youtube