{kind=link}

Alright , folks , welcome back to the Property Couch podcast and have we got a great episode for you today , as we have the winter series well and truly in the rear vision mirror , we are pivoting to the Australian housing market and our mid-year update , ben .

That's right , Bryce . We talk about a water wheel . What's that ? We also talk about economic activity and supply and demand drivers in the property space , and you'll ultimately work out by the end of the episode . Should I act now or should I keep my powder dry ? Hmm ?

folks , good stuff in today's episode . Let's rip into the show .

Welcome to the Property Couch where , each week , you get to listen to two of Australia's leading property and money experts Bryce Holdaway , co-host of Location Location , location Australia on Foxtel's Lifestyle Channel and co-host of Escape from the City on the ABC .

And Ben Kingsley , chair of Property Investors Council of Australia and a back-to-back winner of the Property Investment Advisor of the Year Award , and both are partners of the multi-award winning Empower Wealth , co-creators of more the Freelife Style Design Act , as well as best-selling authors of the Armchair Guide to Property Investing and Make Money Simple Again .

Stay tuned as they bring you the Insiders Guide to Property Finance and Money Management .

All right folks , welcome back to the Property Couch podcast and , of course , welcome back to you too , mate . How are you ?

Tom Stoke . What a great winter series that we had , but now we're sort of getting back into a bit of an update in terms of what's happening in the market today . Pies had a win over the weekend , so I mean , you know , what else is there to sort of talk about really ?

Well , mate , the number one show in town is the Matilda's . And what an amazing force . That team has been right . Their ratings have been building . They're now the most watched television program bar none this year .

And I must admit , ben , I'm not a massive fan of the round ball game , but my eldest son is , and I can promise you I've been caught up in the infectiousness of what's been going on . But it is the Matilda's have given me a love for the game . I didn't know he'd exist it , and I must have been .

I've enjoyed being a part of the group energy that is running around this country about this team that is doing incredibly well .

Now , obviously we're recording earlier than the results , so you know we don't know what's happened in the semifinal , so as you're listening to this , we might have won or we might have lost . We are definitely pre-recording today , so good luck to them if you know at the time that we're saying it now , but we'll know the result by the time you get to listen .

Hey , ben , tell me if you've had a more stressful 20 minutes in your life this year or extended out for 24 months , if you like during that penalty shootout where we thought that we had the chance to do it with Arnold and Mist and then just back and forth . I must admit I can't remember an adrenaline feeling like that for some time .

Yeah , I mean , it's obviously a horrible way to end a game that was so , you know , competitive and so evenly matched , and but , to your point , it does make for great theatre . And so , you know , for the pressure on them , you're just happy for the girls , right ? You're just happy .

They've dedicated their lives , they're playing in the biggest , you know , sporting event in the world right now and they're doing wonderfully well , they're representing themselves beautifully and obviously , you know , from our point of view , we're vicariously living through their experience and it doesn't get any better in that . So it's been a wonderful run .

Who knows if it's continuing , yes , as this goes to air , but even then let's say , if it doesn't , what a magnificent , you know , representation of themselves . And also , you know , from a country point of view , we're super proud of them .

And so , you know , god bless them in terms of everything they've done and , you know , go forward and they can build on this momentum either way , right , thank you , thank you , matilda , for taking us on an emotional journey .

That's been a lot of fun . Just on that too , ben . We had the Winter Series , which , for a lot of those guests , was an emotional journey also . I just want to shout out now to Adam , lorraine , jason Miller , tom and Jody Thank you for everything that you shared and the transparency that you offered , ben .

Part of the goal for us was to give our audience , because there's a lot of doom and gloom around at the moment , but just to remind the community that there's some people out there that they're actually investing during the highs and the lows and the challenges and the discretionary spend squeeze and all those sorts of things . And a little shout out to Lorraine .

I remember chatting to Lorraine and she said oh , I'm not sure my story is worth telling . Well , I can report back that one of our team gave me some feedback , that someone heard Lorraine and said if Lorraine can do it , I can do it and therefore I'm going to actually take the action .

So these people inspire action from our community and I guess our podcast is really synthesized down to one action well given in a way , there . But one thing that we're trying to do , ben , is to get people to take action , and so if it inspires other people to do something so that in a decade's time they can look back and go , I'm glad I did .

That's the whole goal . So thank you . Winter Series we will do a shout out for Summer Series . So if you're hearing that and you think that you've got a story to share , we've got some people already lined up for that , ben . But what I do love is the feedback that we get .

The people say thanks for putting those on , thanks for letting us hear stories of real people who are doing this stuff , which is wonderful . You hinted earlier too , ben , that we are going to pivot . We're going to pivot from everyday stories . Now we're going to get back into some market commentary .

Back in February this year , you and I had a lot of joy at bringing out our crystal ball , ben , and trying to predict what we think was going to happen for this year . We're now going to circle back to that and do a mid-year update on the property market , the housing market , a bit of a touch on the economy as well .

So we're looking forward to doing that today too , ben .

Yeah , really looking forward to it . I mean , at the end of the day , there's always opportunity . We're a believer that you invest when you can and you hold for the long term and you just let it play out . But certainly in terms of what's happening right now , we all suffer from recency bias and what's influencing our mind and our decision making .

So we do need to check in from time to time and so a little half-year update where we can sort of read the tea leaves to Bryce's point , have a look at some of that macro and then sort of give you some of our thinking around where we see it going , both in the short , medium and longer term .

And we're going to tell you about the things that we got right , ben , and we're also going to tell you about the things that we got wrong . So stick around for that as well , so you get a bit of an idea .

But hey , look , for the last six weeks , ben , I haven't had to do my mindset minute , so we put a little bit of a pause on the art of spending anecdote series . So today we're going to pick it up at number nine , which I think is probably my most favorite concept that I have learned from Morgan Housel . I've thought about it a lot .

I've had many conversations about this , ben , from the psychology of money it is . Do you know , when you read a book and at best you could probably hope to have two or three key takeaways from a book you don't remember everything . This is definitely the number one that I remember from that book .

So number nine is no one is impressed with your possessions as much as you are . So if you see someone driving a nice car , really do you think , wow , the person driving that car is so cool . Because that's not what's going through your head .

Instead , if you see someone driving a Ferrari or a Lamborghini , what you probably think is wow , if I had that car , people would think that I'm cool .

So it's a paradox , because people want wealth to signal to others that they should be liked and admired , but in reality , those are the people who tend bypass admiring you , not because they don't think that wealth is admirable , but because they use your wealth as a benchmark of their own desire to be liked and admired .

So it came up with this concept of the man in the car paradox , ben . I'm sure you remember it . I really would love everyone in our community to remember this , and I think it is a fundamental foundation of understanding what it does to build wealth . And here it is it's the man in the car paradox .

People just want to be the person in the driver's seat , but when you see someone in the driver's seat , you don't actually admire the driver , you just imagine yourself as the driver . So if respect and admiration is your goal , be careful how you seek it .

Humility , kindness and empathy will bring you much more respect than the car that you drive or the home that you live in ever will . I remember Morgan Housel got this because he was parking cars early on in his career and got to notice that .

But isn't it interesting , ben , because it's almost like , do you know , when you go to the theme parks or the house of mirrors and you know how you can see yourself , but it's just got this infinite loop , but all of a sudden the mirror just slightly curves off and so the infinite just slightly disappears .

I kind of think of that when I think of the man in the car paradox , because I look at your house , ben , and I go , oh , I don't think Ben's really cool . I go wouldn't it be cool if I was in Ben's house ? And then I get in there and I've got a friend and they go oh , bryce is in that house . Oh , wouldn't it be cool if I was in that house .

And then all of a sudden it's just this infinite loop of no one's actually at the beginning of the train . It's your house , ben , and we should be thinking you're cool , but unfortunately no one is actually thinking that .

So if people could land the plane on this concept which is why I'm laboring on it I feel like it can take away a lot of the stuff where we get this external validation of the stuff that we have , which is costing us a lot of money , which is keeping us trapped in what we're doing , which means we can't get the lifestyle bodies on that we're really after .

If this concept really lands , ben , it's going to solve a lot of people's challenges around spending less than they earn , putting some of the surplus aside so that they can actually go .

This is what lifestyle I want , and if we realize we're all playing different games anyway , the fact that someone's got a better car , a better house , they might need to be in a job or a social group that requires them to have a better house or a better car , whereas in your life you may have different needs .

So this was definitely the most impactful for me , ben . What's your reflections on it ?

Well , it's a super powerful concept . It drives a lot of buying behavior . Ultimately , when you go into an open home , the reason why there's no pictures of the family that live in there is that they want you to visualize yourself in that particular home .

And the reason why we have all of the shows , that we have these desirable shows it is driving that psychology of wanting more , and that is the capitalist society that we roll in , and so the power of these pools are enormous . It's about where to Bryce's point is , where you settle on enough Right Like .

So if you do want to have a house with a pool and an alfresco area because you're love entertaining and so forth , then definitely strive for that . But the point being is you don't have to have 100 meter pool and you don't have to have a 300 meter . You know , alfresco zone with multiple like you don't have to go over the top .

But that's an element of loving yourself and your internal comfort , as opposed to that external validation that you're looking for from others .

Yeah , well , if you want the 100 meter pool and you want the alfresco and you have the means that allow you to do that , great . But for a lot of people they don't .

They have these aspirational goals where they want to be the person driving the Ferrari or the Lamborghini so that people give them the respect and admiration that they think that they'll get from it . And if people are materially bypassing you , so the very thing that you put yourself under strain and stress for actually doesn't even materialize for you .

If we stop and let the concept land and we reflect on , we go . Well , that's actually stupid . If I'm not getting the very thing that I'm chasing in the first place , why should I do it ? Yeah , and I promise you I am not immune to this folks , I am checking myself . Oh yeah , Human we are human All the time , but I reckon I've come a long way .

I reckon I've come a long , long way on the man in the car paradox and how that's landed for me . So , folks , if that doesn't make sense , I'm going to circle back for it in our life hack today , but I really want that one to land .

So , all right time to pivot , ben Time to give an update Our Australian housing market 2023 , a mid-year update , and it's probably worth reminding our audience what our baseline thesis was . So there was a whole bunch of activity coming out of Christmas . There was a fair bit of talk at the time .

We were only , you know , the cash rate cycle had started in May , so we're clearly not in the same position at that point in time as we are now with the additional increases . There was a bit of money in people's bank accounts . They were having Christmas spending and we were reflecting on the post-Christmas glow of where we thought the property market would go .

And so we had a baseline thesis that we thought at the time . We thought there was optimism to think that the cash rate would sit at 3.35 , but our top rate was 3.6 and then a pause . So clearly we missed that . We were close for some time , but then clearly we've missed that , so we will talk to that point shortly .

But our thesis also said there was an attempt for a soft landing . The labor market will remain healthy . Consumer spending will continue to fall Ben , you'll talk more to that shortly . Our thesis also said we don't foresee a recession , and we also talked to the inflation returning to target over time in 2024 . So that was then , ben , what about now ?

What , what's ? Where would we update our thesis to now ?

Yeah , so there's obviously a lot to cover off there . So let's get with the one of the under estimate where the cash rate landed so and we may still have potentially one more you know sort of rate rise potentially if we get more shock in the data . So the analysis did show us that consumers didn't slow down their spending .

The unemployment rate didn't move higher . In fact , the unemployment rate still sits down at sort of these record low levels as we go to go to air Now that unemployment and jobs data is definitely moving in that direction of it of seeing some stress , so we'll start to see unemployment rise from this point forward . So that's the sort of main one .

The other component of it was we just didn't factor in strong enough that consumers would stop spending as well . They kept spending .

Basically , we assumed that they would slow down quicker than they actually did , and so that's just to this whole idea of this concept that they've missed out during a pandemic period and life is too short and they continue to spend . We should never forget this point .

Right , this is probably , you know , in the back of my mind when you think about this now , always understand that the bulk of the consumers will spend the money that you give them . All right . So society has taught us that . That's why we've got superannuation . So I shouldn't have made that mistake . I should have .

So I've been watching intently in terms of the saving ratios that are out there , and I was seeing those saving ratios fall off a cliff . But still a lot of people that had a lot of free money because money was super cheap , interest repayments were super cheap and ultimately , there was a lot of money that was built up .

And so when you get that and people see money in their bank accounts , they will continue to spend . And so you know and we're not talking about the bulk of the population , but you're talking about almost 50% of the population who can't control their spending and so that was a mistake . I will never make that mistake again .

When I know that there's record levels of money in the system and there's plenty of people who are spending , I will not make that mistake . So that'll tap itself out . And so what we've seen from that point is a situation where that is .

Now we are definitely starting to see people getting tapped out of the market from a spending point of view , and that is really starting to show up in basically consumer spending . In retail spending there's still a pockets . There's still a couple of pockets of area that are problematic for us . One of those areas is in services spending .

So we're definitely seeing still airfares , hotel travel . That's still pretty strong . If we look at where America is at the moment , airfares are down around 18% . Consumers have really slowed down over there . So I suspect that we're gonna see something like that play out over the next three to six months as part of that particular story .

But the other clue at the moment in the recent data that I saw was in terms of basically dining and spending out . That has definitely started . So we're not going out to restaurants as much anymore .

So that whole sort of recreational spending is starting to collapse and so if you actually also have a look at where that's sort of happening across the board , you can basically see in terms of a nice little spending chart that came out from from CBA recently said it's really happening in the 1824s , the 25 to 34s and the 35 to 44 people .

So the people who are continuing to spend are really the retirees right .

And less mortgages , and no mortgages .

They're starting to get money on their term deposits , so their cash is starting to make some money for them . They're obviously they're super . They've got to spend a minimum of 4% in their super , so they are still out there spending as well .

And so the combined nature of those record savings and this older generation of getting access to super this big baby boom appeared . So I should have probably factored those in a little bit better in terms of looking at that spending story , and that is , in my mind , led to why the cash rate got a little bit higher than I expected it to get .

Well , we're going to dive a bit deeper , including the fact that we didn't get the property story wrong , which is very encouraging . So , but before we do that , ben , let's set this up with an analogy that you've been toying and playing around with in your mind , and I think it's a ripper , so I think we want to share that with our community .

Just to set up the discussion today , yeah , sure .

So I think what we're talking about here is when we think about the domestic economy , right ? So the domestic economy is the consumption economy . Usually it makes up around 55% to 65% , depending on where the economy is at .

So this is sort of stripping out mining and exports , imports , all of those other sort of main pieces , but this is the bulk of the economic activity that goes on , and it's also really important because that's also where the inflationary element of that comes in there . So I want this is because it's an audio podcast . We've got the video .

But there's this waterwheel analogy that I just want everyone to imagine . So for those of you who are old enough , you can understand that a waterwheel is basically a huge mechanical wheel that turns and as it turns it collects water and then , in the truest sense , it distributes that water out .

But I want you to think about this huge mechanical waterwheel , all right , and I want you to visualize that there's buckets at the end of each of the spokes on this waterwheel and so as that waterwheel turns , it's collecting water . Now I want you to think about water is the actual money and activity in the economy .

So as the wheel turns , it's collecting an amount of water , which is the money and the economic activity in the economy , and it's then basically collecting that and moving it on right , and that's that economic growth that we talk about Now .

When we think about that , there's a couple of mechanical movements that are going on there and there's a yield or productive outcome of that . The first one is , as the wheel was spinning as quickly as it spins , the quicker it spins , the more buckets that can go into the water to collect the water , so you're going to yield more growth and more activity .

The other thing I want you to think about is the actual level of the water . So when you're thinking about the level of the water , that is , about the amount of money in the economy in terms of , so the higher the water level , that buckets going to collect more of that water each time it turns around .

So that's the way in which you might be able to judge this sort of economic activity and this domestic economic activity . So then I want you to think about monetary policy . Now , it's a blunt instrument and that's been well documented by everyone , but monetary policy is designed to release the amount of water and to also put a break on the wheel right .

So when you're in a tightening cycle , effectively what's happening is you're seeing that wheel slowing down because they're putting the brakes on it , but you're also seeing them take money out of the economy , which is taking the water level down so it can't collect as much .

And that happens because our disposable income for those of us who have got any sort of level of debt is actually taken out of that in interest repayments , and so that's basically what we're seeing .

We're seeing the economy slow down by design , in terms of that wheel has been tightened and so we're not collecting as much water and the speed of that water wheel is actually slowing down considerably . Now there's an important message here , because we're at the very top of that tightening cycle .

All right , so the collection of water is going to slow down , so the wheel is definitely slowing down , but we haven't to the point of the money in the economy . We've still got fixed interest rates , so we've still got a bucket of that that's going to come out . We still haven't seen the full impact in terms of that .

Water level still hasn't reached its bottom , and so that's what you're hearing the RBA sort of saying it's like well , we're just going to pause for the time being because we want to basically see just how much water we're leaving left to collect .

And that's a really important analogy , because what actually happens there is the RBA knows , and economists know , that when you do want to release the break off that water wheel , even though the wheel might be turning a bit quicker , if there's no water to collect it's not going to yield that same level of productivity and an outcome .

So what they do know is when they do release the break , it does take time for that water to come back in . So and they know that there is a lag effect . You'll hear them talking about the lag effect in terms of that . So at some point they're going to turn this wheel back on by doing an easing cycle , because they are definitely in restrictive territory .

They've made it very clear and they want to go down to more normalized rates and so they are going to manage that on the back of where they see inflation going from this point forward . But it's really clear to understand that they will go early on a rate cut If they're confident that they've got inflation down .

They will go earlier because the longer that the break is on and the longer that they're not releasing money and the water level is going down , it's harder to get that economic wheel moving again . So it's really important that we all understand that and hopefully that visualizes that in some simple way .

Folks , how good is that ? That is just a very simple way to get a real understanding of what's going on . We've got a friend two doors up Ben . They just put a pool in .

And so what was interesting is , you put the pool in , you put the hose in Ben , and I can't swim the day that the pool goes in because it takes time for that water level to come back up .

And so I feel like that's just a wonderful way for people to get a sense of what's going on here , because , to your point , sure , the water wheel might be spinning , but if the water level's too low , doesn't matter how fast that water wheel is spinning , it's actually not reaching where it needs to be so at the moment .

That's why the fixed rate cliff discussion has been a big part , but that stuff hasn't flowed through into the level of water to the extent , which partly explains why there's been a pause .

Right , because they understand that where that cliff , they talk about the cliff because there's a big amount of volume of loans coming off , but there's still a heck of a lot of volume still coming that hasn't come off yet , which will actually further drain the pool , if you like , which means that water wheel has got less to go into .

So what on your thinking they're made . And , like in COVID , we talked about the car analogy where all it was was just needed someone to get in the seat because it was fully fueled and the motor was fully tweaked . That analogy hopefully helps our community get a real read on .

Okay , that can start to make sense of the data that's being thrown around and how this is actually working and what impact it's having on the people .

Yeah . So let's build on that sort of water level story , because that is what we're trying to focus in on , right ? So you think about how money moves around the economy . Well , there's lots of ways in which that happens . So the first one you think about government spending .

So obviously we have monetary policy , which is at the whim of the independent RBA , and then you've also got fiscal policy , which is about the money that the governments are spending , because what you're trying to do is you need them in unison .

So if governments spend more , that could be inflationary and that could mean obviously that has a longer effect in terms of the amount of inflation that's in there .

So you're seeing governments being on the mainstream conservative about their targeted spending , and I think that's a good move from the federal government in terms of the amount of money that they're putting in for those most vulnerable in the community . I think that sort of says a lot .

Then you start thinking about businesses and you start thinking about what businesses are doing . So business investment has business investment start to dry up ? And if the business investment continues to dry up , you're starting to see that business demand , business confidence , business sentiment . We're starting to see that sort of play out .

So , even though conditions right now are still okay and that's evidenced in the unemployment rate , you've also got this forward looking view that the governments now and the RBA are confident that they've done an appropriate amount of tightening . That says that that water level for business is going to dry up .

And then they expect they're already seeing it with the consumer spending as well . So that water level is definitely drying up because they can see they're not spending as much because they don't have as much money to go around from a disposable income point of view , and then the unemployment story starts to shape up .

So this is where , if consumers stop paying the prices that businesses offer which means that means that's deflationary . So if businesses can't sell their goods for that higher price , they've got to cut their costs or they've got to look at their human capital , okay .

And if that human capital is asking for pay rises and there's too much of those pay rises and consumers continually keep buying those goods , then we'll have this inflation cycle moving along for longer . So what you've got to see is the businesses have got a couple of levers to pull . They can try and put their prices up .

If that doesn't work because consumers don't buy , then ultimately they've got to look at cutting costs and usually what they'll do is lay off people and that's the unemployment story that we'll also play out as part of that particular story as well .

So there's plenty going on at a macro level , but all roads are definitely leading to a slowing economy by design to reduce that water level and to slow down that flywheel . But to the point we're making earlier , when the pause is on , the RBA does not want to lose as much of the gains that they've made in the unemployment area in the employment area .

So remember their two mandates to get the inflation into two to 3% target range and as high as an employment level that they can get .

So they've said in their forward estimates and their monetary policies is that we are going to take a little bit longer to get inflation back into that two to 3% target range and we're going to do that by trying to keep as much of the employment gains as we've made , which bodes well for the flywheel not completely stalling and it bodes well to fill up the

water level quicker , which means you can get that economic activity happening , you can grow the pie and then ultimately , when you grow the pie , you have more money to be able to go around the economy and you get an ultimately better standard of living and better quality of life with that economic flywheel moving in that really positive direction .

As a side note too , ben , that what's interesting here is the system is more important than the individual within the system . So what does that mean for our community ? The RBA acknowledges that there has to be a dent in employment rights , so , to your point , they're trying to minimize that .

But they've also acknowledged that in order to get inflation under control , there needs to be some collateral damage for people with their jobs . That's just part of the recovery , and so therefore , if people take a step back from that , they go , huh , the system that everyone operates in is more important than the individual within the system . So that's okay .

For people like you and me , or someone who's listing who's job secure or whatever , I think oh cool . But what about the poor person that actually has to be the one that's job needs to be sacrificed for us to get to that two to 3% level ? And they'll be .

And the government's saying , well , you are the unfortunate side impact of the broader thing that's going on here . Hopefully that really jars people , when they hear that , to know that the government isn't here to save everyone . The government is here to save the system rather than the individual within the system .

So therefore , why we've made it our life's work to help people create their own lifestyle by design Ben , so that any government support ends up being the safety net rather than the standard operation that people go by .

If you think of the Trapeze Act , when you go to the circus and you see that big net at the bottom , the pension and being at the whim of a government's support should be the equivalent of that safety net . Because you go and you try and hit the , you take the swing and you hopefully that it lands and everything goes great .

But if , for whatever reason , you don't land , there is that safety net . But I just want that point to land .

Someone has to lose their job for us to get inflation under control and for that person it's life changing and they might lose their house and it might impact their state of wellbeing and it might impact their kids and all that sort of stuff is real here .

Yeah , look , we've said all along that relying on government is not a plan . But you will be disappointed if you do rely on government . Now , what the government has the challenge with is how much of a safety net do they wanna provide and who pays for that safety net ? And the best way to pay for a safety net is to grow the economy .

Because when you , I mean we've seen record levels of revenue coming into government on the back of terrific momentum that we had economically leading in before inflation took off , because potentially there was too much stimulus .

But that just goes to show you that when you get that economic flywheel moving correctly , you have an unbelievable opportunity to then provide those services . If you don't and you still commit to providing those services , you really do stagnate the economy . You stagnate quality of life and standard of living .

So that's why the economy is so important , because it's the driver of everything . And to Bryce's point , unfortunately there are those people who are more affected by these types of challenges . But this is why we spend so much time on telling people don't buy the material things when you don't have the fundamentals right .

Don't start a family until you have the fundamentals right , like , ultimately , if you're gonna have to be reliant on the government , then you're going to really struggle in a wealthier society . So I mean , I know that sounds well , that's just not right and it's not fair .

And everyone has the right to have a dwelling , to get to human right , to have shelter , like I get all of what you're saying . But how do you manage an economy to be able to provide that for those most vulnerable ? Well , the best way to do it is you actually grow the economy .

And so when you go through these cycles and you have to go through them , because we know that inflation is an absolute killer when it comes to real wages and real disposable income over a longer period of time so we must get that inflation level down to that sweet spot .

You know that Goldilocks spot , which is that two to 3% , based on the best economic modeling . You don't wanna go lower than that because again you run the risk of stagflation and disinflation . That gets to a stage where people just stop spending because they're fearful of hyperinflation . So that is the sweet spot .

These guys and girls are amazing in terms of the modeling that they do around that . But that just gives you the full context of what we're trying to talk about here , and I think that's probably a good segue Bryce into the property side of things .

Yeah , well , if we think back to February when we were trying to have a bit of a look around what the property outlook would be , we said what was holding the property market back ? Clearly it was interest rates at the time . But the update from then is now also restricted borrowings right .

So the buffer rate at 3% is still for a lot of people they can't service . We've talked a lot about mortgage prison . So it's interest rates and serviceability challenges which is holding the property market back , despite the fact that in a lot of the markets they've grown on the back of very , very low , historically low average listings during that time .

But we called inflation at its peak , but we definitely had that right . And then we also called that it'd be a lot of belt tightening from here . Well , probably got that , as you've to your point earlier , but we probably called that a little early because the belt tightening didn't happen until a bit later .

But clearly there was a couple of things that we foresaw here .

Well , and I think the other big thing we did say is that you won't know the bottom . And as we were recording that back in February , in the middle of February , we recorded that Literally the results came back three weeks later .

And there's always a lag when you get the full results from the marketplace , because not only do you have the auction results but you also have the private treaty sales and the settlements of those private treaty sales . Guess what ? The bottom was actually February nationally , and so we said it's close .

And we were really clear about that because we had obviously the evidence on the ground .

We were looking at the data , the sentiment around , you know , those people who were looking to take action , and the record levels of low supply , just basically that that equilibrium went out of balance and then ultimately , we started to see property prices grow higher and so we've had a nice run of those property prices going higher . So we missed the bottom .

Now the question is where are we going from here ?

Because with the cash rate at a slightly higher tightening cycle level , that does put a little bit of downward pressure in terms of people to Bryce's point people's ability to actually get money , and also that could mean that the economy is going to grow at a slower pace and that means that there could be a little bit higher unemployment than that we were

originally going to anticipate . So we've got these sort of mixed currents that are going on at the moment where you can say , from a supply side , we've got a developing story and then from the demand side , you're trying to detect the level of demand depth in terms of what you're trying to do in there , and that's definitely starting to show different signs .

So I want to talk to that as we think about the next six months , because I think there is some trends in there from a supply side point of view that are worth talking to , and then start to think about that demand side .

I think that's a good distinguishing point to be about just the immediate foreseeable future versus the longer term . Because dwelling approvals are down in both houses and in units . So we've got a number of people coming to this country , you've got new supply being diminished .

So over the medium term that would suggest that that's a disparity that , from the POV of the property investor , should be excited about . That . That should give you enormous optimism and encouragement .

But what our friends at CoreLogic have highlighted is that there is an unseasonal increase in listings right now and there's a bit of speculation around what that might be then .

But if listings at the moment have typically are playing under not only last year's listings in most areas but also the five year average , the little spike at the moment then could be a little sign that some people have could be a number of reasons been , but some people have been holding on for as long as they can .

But just the additional strain on house help might be seeing that some people are selling out .

Yeah , and I suspect quite a few of those would be selling lifestyle properties and also , I suspect there'll be quite of well , we're actually seeing it in the data that there's a real increase in investors who are actually selling at the moment . So that will be further supported by the PIPA data that we're also collecting as part of that sentiment survey .

But it's really clear that when households start to get under constraint , they start to look at the assets that they can liquidate .

And even though we've been saying to people do whatever you can to hold on , because it's only gonna be a small window in time that this is gonna be an issue , but there's no doubt that we're starting to see potentially those investors who've got a bit greedy , who bought too many properties , who didn't factor in long-term interest rates , going back to more

normalized levels instead of thinking that interest rates are gonna be lower for longer , those people are starting to tap out . And so then you start to think about well , what does that look in the grand context ?

So , yes , we have seen a bit of a spike in the short term in terms of new listing numbers , but overall , nationally , we're still down below that five-year average . And to Bryce's point , this is when you start to think about mechanically the demand that's sort of gonna come into the market .

So we've got low building approvals , which means we're not gonna build as much accommodation . We've got positive population growth .

So from a very , very big macro level , there is going to be a continued under supply measure of the amount of dwellings that we need to accommodate everyone , unless behavior changes , which we're also seeing and what we're seeing in the behavioral changes household formations on the back of COVID , where we basically wanted more space , more freedom , less composition of

households in the formation , we're now starting to see that completely reverse . So we're definitely seeing kids going back and living with their parents to save a deposit . We're definitely seeing share households getting more people coming in because rents are going higher .

So we're just seeing that natural evolution that the market is playing out as we expected it to during this time that when money gets tight , we've got to think about ways in which we solve our own personal challenges around money . So that means , yeah , I used to just have a two bedroom apartment that I rented by myself .

Now I've got a flatmate because ultimately I want to split the rent because the rent's gone up .

That's an important point , isn't it , ben ? We had a housing shortage , but we didn't have a bedroom shortage , and that was where the efficiency gain , or the optimization to your point that you're saying there once we start to get a bedroom shortage , well then we know the market's really really fully optimized .

Yeah . So we then put all of that in and we start to have a look at some of the different market segments and we can see from where we were in February to where we are now .

There has definitely been a shift in the number of properties available for sale in sort of different states and territories , and so we can see , when you look at Sydney by way of example , they had 18,000 properties available for sale at a snapshot that we did in February and now they've got 19,000 , almost 20,000 .

So it's almost the net 2,000 additional properties that are available on market at the moment . We saw Melbourne had 24,000 properties available for sale in the snapshot that we did back then and now we've got 25,000 properties available for sale here . What you're definitely seeing is this is where you can start to look at market . It's in markets .

Perth is one of the hottest markets , right , you see . You see 12,600 available for sale in February . Now there's only 10,300 available for sale . You look at markets like Adelaide , where you've got again 3,900 in February , 3,800 now in August . So there are definitely opportunities in the marketplace for those particular opportunities .

So we are definitely saying watch what's happening with supply .

But I'm definitely not seeing and this is what I'll continue to keep reminding you all when I start to see it , there's no systemic or systematic breakdown in terms of the amount of properties that are coming online for sale at the moment , and so one could argue , as the banks have totally reversed their forecast for property prices , they expect the property prices

to be negative by the end of this year again a second year of negative growth . Now they've actually turned them into the next three years . There's going to be positive price growth in those particular markets . So you can see , now they have richer data , more insights .

We keep it relatively simple here when we're looking at the volume and we're looking at the demand drivers , and we don't get caught up in two super macro stories or the noise going around fixed rate cliffs and all of these other things .

But if rates stay higher for longer , you would expect that there will be potentially more houses , households that will be looking at how they may reduce the amount of properties that they do own , and so that does bring in a little bit of a downside risk .

So it wouldn't surprise me if price growth I'm talking about growth per month starts to slow further and we get back to more of a balanced market in the short term and remember I'm talking super short term , about the next six months .

But then after that which is where where good , smart investors go , they don't think in months , they don't think in a year , they're thinking in a couple , they think in five , 10 , 15 , 20 year cycles that this is going to again be a time where , obviously , when interest rates start to come off their extreme levels of tightening and come down to more normalized

levels might take a little bit longer than normal , but because we've had this record increase , but then that's obviously where you could have confidence that that's going to have a ground swell of additional levels of demand , in addition to the migration and the population growth which will naturally add to demand .

That you've got to be relatively confident that property prices over the next couple of years , subject to no market interventions which we will get to in our downside risk section subject to no silly decisions being made by governments and regulators , that the market and let's hope I mean I don't like this idea that it's boom bust , I just want a stable market where

there's consistent , steady growth .

But we know that's not how buyers operate , that you know they've got this recency bias where they only need to go to two or three weekends of auctions and open homes and seeing property prices move quickly and then they panic and then they have FOMO and off we go to the races again , where we see property prices go really , really high very quickly .

So we don't really like that . That's not where we want to be . Where we want to be is in a okay , it's a sensible market , but with tight stock and potentially interest rates coming down next year . I don't . I just see it playing out as a positive growth story for property again .

Yeah . And if we have a look at what we said back in February just to round that out , ben , you know we asked the question are we close to hitting the bottom ? We said yep , super close , and if we're right , we think the demand hits quickly and you'll miss the bottom .

So we think our self assessment is that we will right there , ben , but folks have missed the bottom . So clearly , going forward to your point , there's that window where there might be a little bit of neutrality around that , but I always just go back to . You know , supply is the enemy of growth .

If we've got under supplied dwellings , we've got lots of people wanting to come here , We've got a rental market that is ridiculous for everyone involved . So you've got all these conditions . Conspiring to suggest that supply being the enemy is so far away from the discussion . It's palatable , right ?

So if you have an opportunity and , to your point , if you're not a fair weather supporter of the property market , you're actually playing a long game .

Chances are if you factor in lead times as well , that it takes to get in there and the time it takes for you to sort out finances , because clearly that's not easy for anyone right now chances are there is an opportunity because if some of those listings come on , where's a buying team are excited about that , ben , because if they fit our criteria , we've been

waiting for those extra opportunities to come , because even if they come off a little bit , we're fine with that , given the fact that where we're planning to go . So we think we got that prediction pretty right back in February .

But the update is your point you just said it just having a look at that pent up demand and what that looks like with this little uptick in listings .

Yeah , and if we can double click on that demand story , outside of just the natural population story , we know that with APRA's 3% buffer rate , which you mentioned earlier , is that is also a throttle on growth and they've been arguing that it's about , obviously , the system stability of the financial service and financial markets .

That's what they're protecting and they don't have an interest in the property story . But their argument for keeping the buffer rate at 3% was about where the interest rates will go . Now the reality is is that if we are at the top or one move away from that , then their argument of a 3% buffer on top of that is actually null and void .

In fact , what they will be doing if they continue to keep the 3% buffer rate , if you think this through , they're actually creating greater homelessness and they're creating to the point we're making about our waterwheel .

By them doing that and not allowing that money to come into the economy , they're slowing the economy down , which in theory , could actually be more detrimental to the economic stability and the financial market stability that they're trying to protect . So they can't argue the point to keep a buffer rate at 3% if the cash rate starts coming down .

So if you think about not only a cash rate movement down but a movement by opera of , say , half or 1% each point down . That is going to trigger probably a 10 to maybe 20% improvement on borrowing power . And that is again another argument to suggest that property prices could move higher in the new year .

And I would be staggered if the if opera could come up with an argument to want to keep that buffer rate at 3% . I understand behind the scenes why they would do it , which is , you know , property prices could be inflationary . Right , there's an inflationary story there .

So you know the opera sorry opera and RBA and treasury might be sort of manufacturing that behind closed doors in the Council of Financial Regulators that they're worried about the inflationary element of that . But to counter that , if you don't get that supply into the market , then rents are going to keep going higher and that's inflationary in itself .

So I think the best way to look at this is let the market do its work , take the regulatory element out of the market and let the marketplace work itself out , because that is naturally going to increase the supply and we all know that supply is the enemy of value or price . So if you want to bring prices down or make things more affordable .

You'll ultimately need more supply .

Well , okay , let's talk to that point . Then , ben , the downside risks of you know going forward . I am , I am , do I really want to poke the bear is what's running through my head here with you . But let's talk about what some of the downside risks are .

And what we see is the biggest risk , ben , and that is market intervention , government market intervention .

Yeah , right now the Greens are running a very , very strong campaign to look at a two year rental freeze across Australia , and we know , obviously , that there was a meeting yesterday , so we'll talk about that meeting at , you know , the next pod once we get an update from the National Cabinet in terms of what that story looks like .

But this is a this is a real battle , right ?

This is basically a battle between effectively the Greens positioning that rents need a better deal , renters need a better deal and , and ultimately , the property owners should be able to subsidize their rents , and so that in itself would be unprecedented in terms of small businesses having to subsidize their tenants in those properties .

So that is hopefully , you know , smarter minds will prevail .

We saw last week Governor Low , who's who's , from my point of view , one of the best governors we've ever had , really make it clear that , you know , in terms of restricting or introducing any type of restrictions and interventions in the property spaces , unproductive , it's unworkable , it's going to have long term unintended consequences .

So so I think , hopefully the smart people inside Treasury and ultimately would be advising the politicians that they shouldn't introduce that particular policy . So you're thinking about that , you're thinking about APRA causing that unnecessary restrictions on borrowing which will , you know , again , restrict supply . They are the two ones .

And then the final one is about stubborn inflation . So we haven't talked about inflation a lot yet in the pod , but I'm sort of thinking about that . There is a risk of that right .

Ultimately , if employment stays stronger , if we see wage price spiral risks on the services side of inflation , then you know that that could be problematic and we know that stickier inflation we said it earlier it's a killer for economic activity and it means we have to have higher interest rates over a longer period of time , which you know .

That water wheel , the economic flywheel that we're talking about , that you know . Slowing that down , you know , for those of us old enough who knew how hard that wheel was slowed down in the early 90s with the recession that we had to have , I can tell you that is unwelcome . You were talking about unemployment , sort of pushing through into sevens and eights .

It's just not a place you want to be . And so they are the downside risks when it comes to the broader economic market , which has a flow on effect obviously into the property market .

Stick around to what's making property news folks . Ben and I are going to talk to this point at a satirical level shortly , but I think it's worth just laboring on this point .

Ben , it was part of the submission that you did on behalf of Pica around changing the narrative We've talked about it briefly before but changing the narrative for property investors as , instead of the greedy fat cats who are getting all these negative hearing benefits that make the headlines , seeing them as the small business owner as you'd have the food vendor small

business owner , or just think of anyone in your world or anyone who's listening to this as a small business owner they are taking an element of risk with , ultimately , the hope of a return .

Obviously , if they've probably taken a loan against their home to fund that small business , they're trying to create equity in that small business through retiring the debt and creating some goodwill .

If they've been lucky enough in their small business and their skills as a as an entrepreneur , ben , they might have actually then branched out into a second location or a second business as a small business owner .

But I think you know most people in the community wouldn't be labeling small business owners as fat cats or people that are leveraging the tax system in order for them to get ahead . They're actually creating employment , having a swing for a lot of small business owners . They don't turn over more than a million dollars .

A very high percentage of small business owners don't turn over more than a million dollars in revenue . So it's not once they factor in their margins and the stress and the . You know they're not .

If we can change the narrative for property investors to be the same as that and this is , you know , I'm borrowing from a lot of the good work that you and the team at Picker have done .

I think that's helpful because if you have a look at the list of property investors in this country , yes , you will see a lot of high paid , typically health professionals at the top of the list . But if you go past that , ben , so okay , so they're high incomes and they've got an advantage .

But if you go to below the top 10 , right through to the top 200 occupation , there's public servants , there's school teachers , there's nurses , there's there's a whole range of cross-section of society where no one would say , oh , they're greedy , fat cats .

So again , I think we're getting lost in a narrative that we're not in control of , that's seeing us as fat , greedy people who are living off the the negative gearing narrative .

But if that can be changed quickly , then the unintended consequences that we fear from that narrative is that well , the problem gets worse before it gets better if people can't jump onto that . So that's that's why it you know I said it pokes the bear with you .

That's why we spend a lot of time talking about this , because if , if market intervention is continually played with by governments , there will be those unintended consequences that are not good for anyone , even the people that they're trying to protect .

Well , an interesting fact , bryce in the ATO data , nurses and teachers are in the top five , the top five of property investors , investing owners . Now they are basically making a decision to sort of say look , I may not earn high incomes in my chosen field , but I do job for purpose and return for society .

They've got very limited options in terms of how they then create self funding retirement and this is their small business . This is the way in which they do it in terms of the passive small business . So that just gives you a bit of a highlight . So , but they're the downside risks . Let's , let's now turn to the upside opportunities .

So we do know , just with a couple of months of pauses , that that has a positive sentiment effect on the marketplace . But if we think about what's around the corner , and that is an easing cycle , that is also going to have a significantly positive impact on sentiment and that will stir up the depth of demand in the market . That'll be the first real test .

And to Bryce , and my point is you want to get in before that . You don't want to wait for that . You're crazy if you wait for that because you've just got to pay $100,000 extra for the property that you could have got now , so . So that's really important .

I know I'm giggling , I don't know why I'm giggling , but I don't know how else to just stress the point that you need to .

Into the turd mentality , Ben , because we know that most people will ignore what you just said . Most people will and then , on the other side of the event , they'll go . Well , geez , we should have done it earlier . So that's the explanation for the giggle . Like you , just you've done a couple of laps around the sun and know what's coming .

Yeah , exactly . Well , that's that experience right ? So then obviously solid employment is really important . So we don't want people speculating in property , so you want to make sure that your job is really secure , that the industry that you're in is a growth industry , because property investments for the long term .

So if that's you great , then obviously you've got that strong surplus still coming through and you understand that rates are going to come down , which means repayments are going to come down , and you've got a comfortable buffer .

Then it's it's crazy for you not to be thinking about how you can take advantage of this particular market , because rent side looks good , population growth looks good , all of the fundamentals , the under supply in the marketplace looks good . So when you're thinking about all of those types of things , that's really important .

The final upside thing for me is really about borderless investing . So if we do see the Andrews government in Victoria potentially lose their complete minds I don't think they're far off , but let's say they lose their minds completely and they do try a rental cap or a rental freeze in Victoria , then mark my words investors will vote with their wallets .

They already are . You're already seeing it , since they introduced 133% sorry , 133 different reforms . In fact , I'll I'll even put a . I'll see if we can put a link into it . I did a bit of a research on that and posted something on Twitter last week , but I might throw something up on LinkedIn and see if the team can share it around as well .

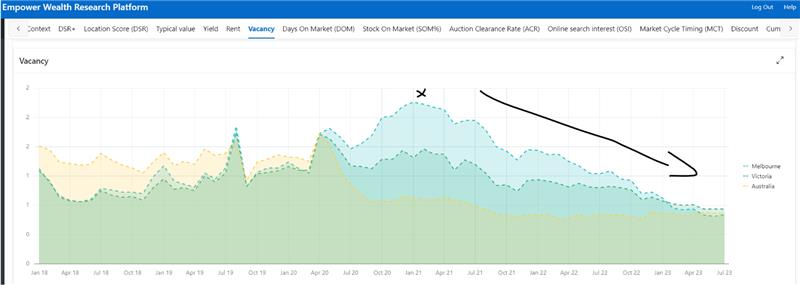

But it's just clear . It's clear as day that basically available well , vagancies are falling through the floor in Victoria because investors are just sick of it . They've just had enough of the way in the Victorian government treat investors down here , so that that in the short term , is going to be real .

If you are an investor in Melbourne , please I want to say to you like , think beyond this Andrews government . They will be booted out . They will be booted out , but it's still potentially not a time . You know , be greedy when others are fearful . I get that statement as well .

But there are people , just on principle , who will sell up because of the way in which they're being treated down here in Victoria . And I say , be careful what you do . I mean , I know principles are , you know , are a good thing , but ultimately , you know , think about what you want to do in the Melbourne market attached to that .

So I'm not saying get out , but I know people will . We're already seeing it in the data . So , but be a borderless investor . So the next one you buy . If you're thinking , you know , for opportunities in the market for short term growth , you wouldn't be looking at Victoria as part of that or Melbourne for the time being .

But if you're thinking medium to longer term and being greedy when others are fearful , that market remains open for you to consider as well .

And a play on the greedy . When others are fearful , ben is be opportunistic when others can't . So what that means is , if you , if you're in a fortunate position where APRA isn't throttling you and you can get access to lending , well , there's the opportunity that exists for you .

You have a , you have a unique position where you can get access to , to the money to be able to go and transact in the market , because , as soon as the rates do come down , you won't be alone . You'll have a few mates lining up with you .

There'll be a lot of people at the auction . There'll be a lot of people putting offers in . Yeah , that's true , very good .

All right . So we've talked about the downside risk spend . We've talked about the upside opportunity . Now it's time to talk about who shouldn't play , who should sit tight , who should sit on their hands , even though you will miss this buying opportunity .

We'll give you reasons why , and the first one is if you want to buy investment property , it's buy the right property , correctly .

Finance it when you hold it for the long term , when your cash flow allows , when your cash flow allows , is the important point we want to lean in on here , because that's two parts One , you've got to have a buffer to make sure and some surplus , but two , you've got to make sure that there's continuity of that .

So if your job is not secure or if you're feeling anxiety around that , this is a time for you to sit on the side of the line . Then do not proceed , do not pass go . You do not want to put yourself into a position where your household is under strain .

Yeah , I think we keep repeating that . The classic ones job security , cash flow management , all of those fundamentals . Unfortunate that those people who already have too much gear in can't also add to their portfolio if they wanted to as well .

The mainstream media is going to have multiple stories of boom bust , so basically , completely take them out of your consideration in terms of what that looks like .

And for me , the other ones who are going to start coming back out of the woodwork are the spruikers who are going to be looking at selling you big tax incentives and telling you these are the sort of things you're looking for .

And if any of them are offering you a rental guarantee , for God's sake , run a mile , because if there's ever a market that I've been in in the last 25 years of doing this , you need a rental guarantee . Have a look at the vacancy levels , like AR and Chrysler . So if you sign up for a rental guarantee , it has been priced into the price that you pay .

So from my point of view , again , continue to avoid new and off the plane . You know house and lands . They are not necessarily going to be where they need to be , but if there was a time to buy house and land .

You know , if I was ever to sort of , if you were ever to convince me that a house and land in a tight location where there's not ample supply of land , this might be one of those very , very rare occasions , but I still wouldn't do it , you know .

I mean like I still a bunch of folks about to say Ben said yeah , I still wouldn't do it , even if you said , well , that's lining up . You know there's people who want to buy , that's lining up . You got record population , that's lining up . There's an under supply , that's lining up . Yep , still wouldn't do it .

I'd buy existing and I just buy for the land value focus that I've always said you need to do . So that just gives you some idea of where our headspace is at . So , rounding out , we love Perth , we love Adelaide , we love pockets of Southeast Queensland . At the moment , again , it's markets within market story .

Sydney is going to cool off a bit , melbourne's going to cool off a bit , but if you're playing the long game , those two markets should always be in your portfolio . Yeah , that's right , there's the opportunity , you're right , there's the opportunity . And then you've got , obviously , hobart , no is a no for us .

Darwin sort of oh Canberra is definitely a no for us . They've just , you know , again put pricing caps on rent . We would never go into Canberra . Canberra is a market where you've got a government who you would never trust . So you don't . You know , you need to have continuity in your governments in terms of looking .

So they are going to have massive problems with rental accommodation over the next 20 or 30 years because they just simply are a pro tenant versus pro investor and owner . And so I would avoid that market like the plague . And then you've obviously got , you know , those other supplementary markets which are the regional markets .

But to my point , I think that's a bit counter cyclical in those particular markets at the moment You've got enough to buy in in terms of Perth , adelaide , southeast Queensland , melbourne , sydney , canas cyclical , and if you're a little bit more aggressive , darwin's going to be an interesting market to watch .

But excuse me , but I'm , you know , I'm not putting my dollars there .

All right , folks . So hopefully that's given you a bit of a . Hopefully it's given a little bit of a sense of calm in the marketplace . We've covered a fair bit . We talked about the water wheel analogy . Hopefully that lands field love for you to go and listen to that again . Feel like that will really help the plains land for you .

On what's going on here , we've talked about where we think interest rates are . Clearly we're super close to the top . Is there another one ? Who knows ?

But if you have your cash flows and your buffers in place there and it's part of a bigger plan for you , we see that there may be some opportunity here for you , given supplies tight , not only in supply of new stock , also in terms of people trying to rent properties .

So we still see that property demand increasing and all you need to do is have a look , folks , over the next two to three years to see how many people are landing here , how few , what the shortfall in the number of dwellings for those people that are landing here , plus the natural internal demand that we create Organically for that property .

So properties still a good story , and we've also told you what the risks are .

Hopefully you get to consider that when you decide whether you want to proceed or not , we've talked about what the upside might look like for you and we've very clearly said to those folks whose job is insecure and you're already under enormous pressure in your household Now is not the time for you to play .

Now is the time for you to stabilize what's going on in your own homes so that you can get to the bottom of your house , so that you can get yourself into a position where you sleep with both eyes closed and obviously get yourself into a position where you can get some surplus and obviously act on that going forward . So stick around , folks .

Ben's got what's making property news coming up . We'll talk a bit more about the current market , but then my life hack today is I would love for people to do a man in the car paradox audit in their own life .

Think about your friends , their car , their house , their holidays , and I want you to really think about did I actually wish I was them or did I wish I was in the situation that they were in to get the admiration that I think is coming ? I think the man in the car paradox audit is something that we should all do . I'm reflecting on that .

So , and if that becomes conscious spin , then all of a sudden you can start to go . What can I eliminate in my own life ?

Where I'm actually trying to impress my own friends when they're not going to be impressed at all anyway , but it's putting me under stress , where I'm spending more than I earn because here's the , here's the thing that I promise you folks in my 48 laps around the sun is that they won't notice , they'll be too busy trying to impress you or someone else back .

So if you , if you do that , think about the House of Mirrors analogy that I talked about before and have a think about will this improve the quality of my own life ? Will it actually increase the amount of time that I have with my loved ones ?

Will it actually reduce the amount of stress that I put on my own household budget because no one's actually looking in the first place ? So there you go . Man in the car paradox audit , give it a go . Hey Ben , what's making property news ?

Well , mate , obviously we've been in winter series so that you know we haven't been talking a lot about the marketplace in itself , but it's it's the season of inquiries price . So right now in Victoria , the Victorian State Government has a rental and housing affordability crisis inquiry .

We've submitted our paper to that and I've been asking to attend one of the live events for that . They haven't invited me yet . I'll continue to keep nudging them .

I might even have to take that one to the media , because it does just look like it's a talk fest for renters talking about their rental increases and not necessarily getting the context from what the costs have gone up for the homeowner .

We've got in New South Wales also an inquiry that closed that was around the same sort of thing in terms of a review of their tenancy reforms , and so at the moment they don't have a no grounds clause termination that we have in Victoria , and so that's been the real killer for the Victorian appetite for investors there . So there's that inquiry .

So , if you want to , we'll put in the show description some links to these inquiries so you can look at some of the submissions and also potentially put your own submission in .

And the final one , bryce , which is where we want to spend a fair bit of time is there is an inquiry in the federal government , inside the Senate committee area , and effectively what this is . It's inquiry led by the Greens . The terms of references are basically 100% loaded towards how the tenant is being impacted , how the renters are being impacted .

So it's a political stunt and we are definitely seeing the Greens propagate misinformation or disinformation in certain areas around that and so . But their strategy is this they want they want every tenant and rent to put effectively a submission in to that inquiry , and so they've extended the original time period to the 1st of September .

And so the Greens spokesperson , max Chandler Mather , I think his name is he has actually said you know , the more people that supply their submission to that , we will be able to out trump and basically put a lot more pressure on the government when it comes to lobbying for a rental freeze for two years .

So the counterbalance for that is is we're going to do the same . We're calling out to all of you in the show notes to put you to put inside this your submission .

I just want you to do this really simple thing Put a submission in , just tell them how much your costs have gone up , from whether it be interest rate costs , whether it be your insurance premium costs , whether it be your compliance costs because of all these reforms that are going in , whether it be higher taxes and charges in terms of land tax rates , the

things that are being introduced levees in Victoria that have been introduced . Tell them how much your costs have gone up and then tell them how much you've passed on to your tenant . Right , that is all I want you to do . You don't need war on peace . Just basically say here's what my costs are being .

This is basically what I've been able to on charge to my tenant , because that is that in itself is going to be the weight of evidence . That sort of gets gets this conversation away from . Rents have gone up . They have gone up , we totally agree , and it's not great for some households . We understand that completely as well .

You know people are being impacted , but the property owner , the small business , has had a massive increase in costs and so they are not talking about that . They refuse to talk about that . They refuse to claim that there's price gouging going on when they get the full facts . There's no systematic or systemic price gouging going on .

This is the vast majority of property owners , small businesses who are allowing their property for lease and quiet and safe enjoyment , are basically covering , recovering some of their costs . So , from my point of view , that's the action that I want all of our community to take .

If you're a property investor and you have been impacted negatively In terms of cost , tell them , because it really is important , because all they're getting is one line of one line of input , which is oh yeah , my landlord put my rent up $80 a week .

There's got to be some context and there's got to be some balance in the conversation , and that's why it's really powerful that we do this . What's making property news section section , because we need to act on it .

Yeah , and it's you and I had a little tongue in cheek the other day because we watched that video from that greens and it's like imagine if , imagine if it's the same thing .

You know the fish and chip shop and and I'm I'm the person you can't put your fish and chips , the price of your fish and chips , up for the next two years because the poor people who are eating the fish and chips , it's not fair that you increase the prices to them .

Yeah , you need , you need to subsidize my minimum chips . Yeah , like you know , I enjoy my minimum chips and all you've been doing , like you know , this is . His argument went like they property investors already get too much . They already get $39 billion in concessions and obviously I took that to task .

Those concessions are exactly the same as every other business owner in the country gets and any other investor . If you invest in shares , you get a 50% capital gains exemption if you hold the asset for greater than 12 months , and the other that the other amount that made up the bulk of that $39 billion was interest expenses .

So basically what he's saying to all of the people who are listening is they get $39 billion in concession . Imagine if you said that for other small businesses and big businesses , everyone can claim their costs as a deduction against their income . Why is it now bad that property investors aren't allowed to claim those costs ? So it was just obviously disingenuous .

It's obviously politically motivated . The Greens are interested in getting more members into their , into their camp and this is doing very well for the you know for them in terms of their political agenda . But in terms of whether they really wanted to actually add to the supply of property .

Then they'd pass the federal government's $10 billion package to get more properties built , but they continue to not do that because it's a political advantage for them in terms of attracting new members to their political group .

And , of course , a shout out to all of the Greens supporters listening to us and the Labour supporters .

Ben , our agenda is largely around housing policy and around our area of subject matter expertise , so we get that some people disagree with our political views on who should be in and who should be out , but what we're saying here is the agenda behind the parties that they're pushing .

We think will have unintended consequences , which we have talked about a fair bit on here . But I think hopefully the biggest takeaway for everyone today and it was the biggest part of the submission , ben was the reframing of the discussion .

I think it was brilliant is to is to start the conversation and be really wonderful if journalists who are listening to this could start the conversation around that too , that property investors are small business owners . I really think that will change everything , rather than seeing you know like you said , oh , they put my rent up 80 bucks .

We don't want to get into a situation where we're disincentivising everyday property investors to the top end of town . So they do the whole big built to rent schemes and the big corporations and the superannuation funds are the ones that get all the advantage and the people who try and have a swing at self funding retirement , lose all their strategic advantage .

So , but just just for those folks , ben , who are Greens supporters will just . We'll just throw it out there that it's about the policies .